E-commerce Conundrum: Shrinking Profit Pools and the Perils of Premature Success

Deep dive on e-commerce models, profitability and understanding the competitive landscape in South East Asia

E-commerce as a sector has existed for more than three decades now and has evolved into multiple formats that we see currently including horizontal platforms (Amazon, Flipkart, Alibaba), vertical platforms (Myntra, Nykaa, Zalando), social commerce (Meesho, Pinduoduo), multiple D2C platforms, and B2B platforms (Udaan, Shopify) and numerous other formats.

Understanding the different E-commerce models

However, all these different formats broadly operate under two core business models:

1P (First Party): In a 1P model, sellers sell their product directly to the platform (buyer) and the platform then in turn sells the products further to customers. The platform (Amazon/Flipkart) handles the logistics, advertising, inventory etc.

3P (Third Party): In a 3P model, sellers sell products directly to consumers on the marketplace. They have control over the advertising, marketing and other logistics of products, including shipping. However, they can still choose the platform’s fulfillment services if they wish.

Now from a platform’s perspective, let’s evaluate the pros and cons of both models.

Contribution of 1P vs 3P in major e-commerce players GMV

Key Accounting Difference in the P&L (Profit & Loss) for different models

1P transaction: Revenue = GMV.

3P transaction: Revenue = GMV x Take Rate (or “Commision).

There is another major distinction between 1P and 3P transactions: Inventory.

In a 1P transaction, the cost of merchandise is recorded in COGS (Cost of Goods Sold)

In a 3P transaction, there is no inventory cost recorded with a sale as the platform doesn’t buy the product from sellers and doesn’t hold inventory

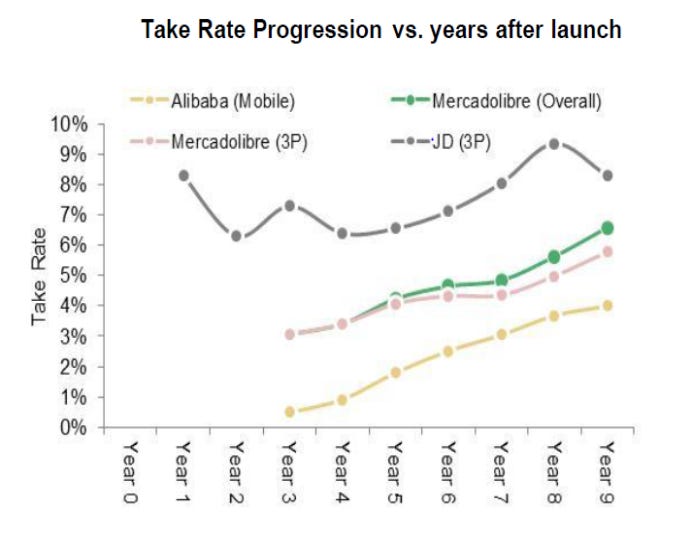

Take Rate Comparison of Major E-Commerce Players

Note: Given the cost of selling is usually around 6-7% of GMV and sales & marketing, G&A expenses account for another 4-5% of GMV, anything less than 10% take rate will never see the light of profits.

This begs the question of marketplaces being able to increase the take rate or commissions beyond 12% in emerging markets.

E-commerce - The lost darling sector of investors?

Historically, e-commerce as a sector has been a favorite for investors and companies have raised billions of dollars given the huge market growth opportunity specially in emerging countries such as India and Indonesia.

E-commerce is the key battle zone where several Chinese platforms appear to be excited about prospects in ASEAN, but the market reality seems to be different. The growth has markedly slowed down post the jump seen during the Covid pandemic and in the long term, it seems to be a low-teens growth market with lower profit pools compared to developed markets, ensuring lower margins.

The perils of showing profitability

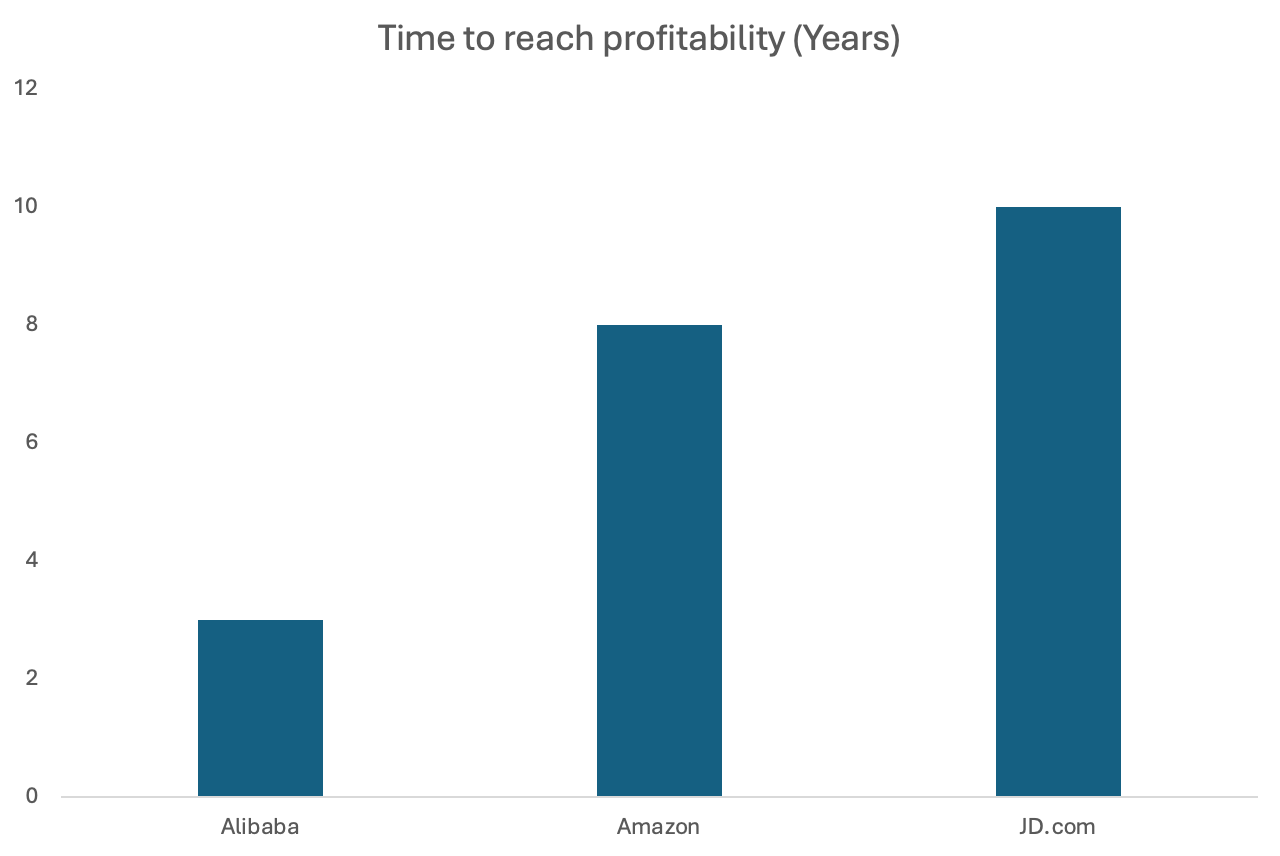

The initial e-commerce pioneers reached profitability within 6-7 years since operation on average, however, that timeline seems to be getting shifted further and further in recent times. Flipkart, for example, has yet to show any signs of profitability despite being operational for more than 15 years.

Shopee (Sea Ltd) turned profitable last year after 8 years of operation, however, unfortunately, that did not last too long and the company turned into red again after showing profitability for a few quarters.

Can e-commerce companies in India or Southeast Asia show consistent profits?

While E-commerce can be profitable in emerging countries, as Sea Ltd demonstrated, but showing profits is dangerous at this relatively lower penetration of online commerce, as it can quickly invite competition. Sea Ltd realized it and quickly pivoted back to an investment mode turning into read again.

Endless funding appetite and deep pockets by large companies reduce entry barriers into new markets and segments. Chinese platforms, in particular, are making their mark on a global scale, displaying a strategic vision that spans much larger time period vs the typical 7-year cycle for private equity or venture funds.

Surprisingly, the lack of immediate profitability and the relatively modest market size do not deter these giants given the high profitability in the core segment which can fund the cash burn in newer segments in search for growth. Unfortunately, this favorable scenario is not replicated for smaller, independent platforms that originate from the India or ASEAN region with limited funding from investors, leaving them without the same financial safety net and eventually leading to a larger cash burn to gain market share and thus, entering into a vicious cycle.

Increasing competition from Chinese players

India banning Chinese platforms was a strong regulatory move that further pushed these Chinese conglomerates to Southeast Asia.

Tiktokshop: Tiktokshop is estimated to be targeting a $50 bn GMV in 2024 and while a large part of growth is expected from the United States, one can not rule out the possibility of increased competition in ASEAN. The company is already estimated to have around 10% market share in Indonesia, Philippines, Malaysia, Vietnam, and Thailand.

TEMU (Part of Pinduoduo): Temu’s is also witnessing rapid growth and is bringing a wide range of lower-priced products through wholesale merchant relations in China/Korea along with free marketplace (no seller commission) and relying on 3PLs for logistics. This can drive down take rates in geographies further impacting the unit economics of incumbent players.

Thanks for reading. If you found this insightful, please like and share it with your friends and subscribe.